On January 10, 2022, the Circular 1/2022 of the National Securities Market Commission was published in the Official State Gazette (Boletín Oficial del Estado), regarding the advertising of crypto assets presented as investment products (hereinafter, the “Circular”), which we will comment on in this article.

Article 240 bis of the Royal Legislative Decree 4/2015, approving the consolidated text of the Securities Market Law (hereinafter, “LVM”), introduced by Royal Decree – Law 5/2021, on extraordinary measures to support business solvency in response to the COVID-19 pandemic, grants the National Securities Market Commission (Comisión Nacional del Mercado de Valores, hereinafter, “CNMV”) powers to subject to administrative control the advertising of crypto assets offered for investment purposes.

TABLA DE CONTENIDOS

- 1. What is the purpose of the Circular?

- 2. Essential definitions of the Circular to be clear about

- 3. Objective scope of application of the Circular: advertising activity for crypto assets that are the object of investment

- 4. Which crypto asset advertising activities are excluded from the objective scope of application of the Circular?

- 5. Subjective scope of application of the Circular: obliged entities

- 6. How should obliged entities conduct advertising campaigns for crypto assets?

- 7. Is prior notification to the CNMV required to carry out advertising activities on crypto assets that are presented as products of investment?

- 8. Evaluation

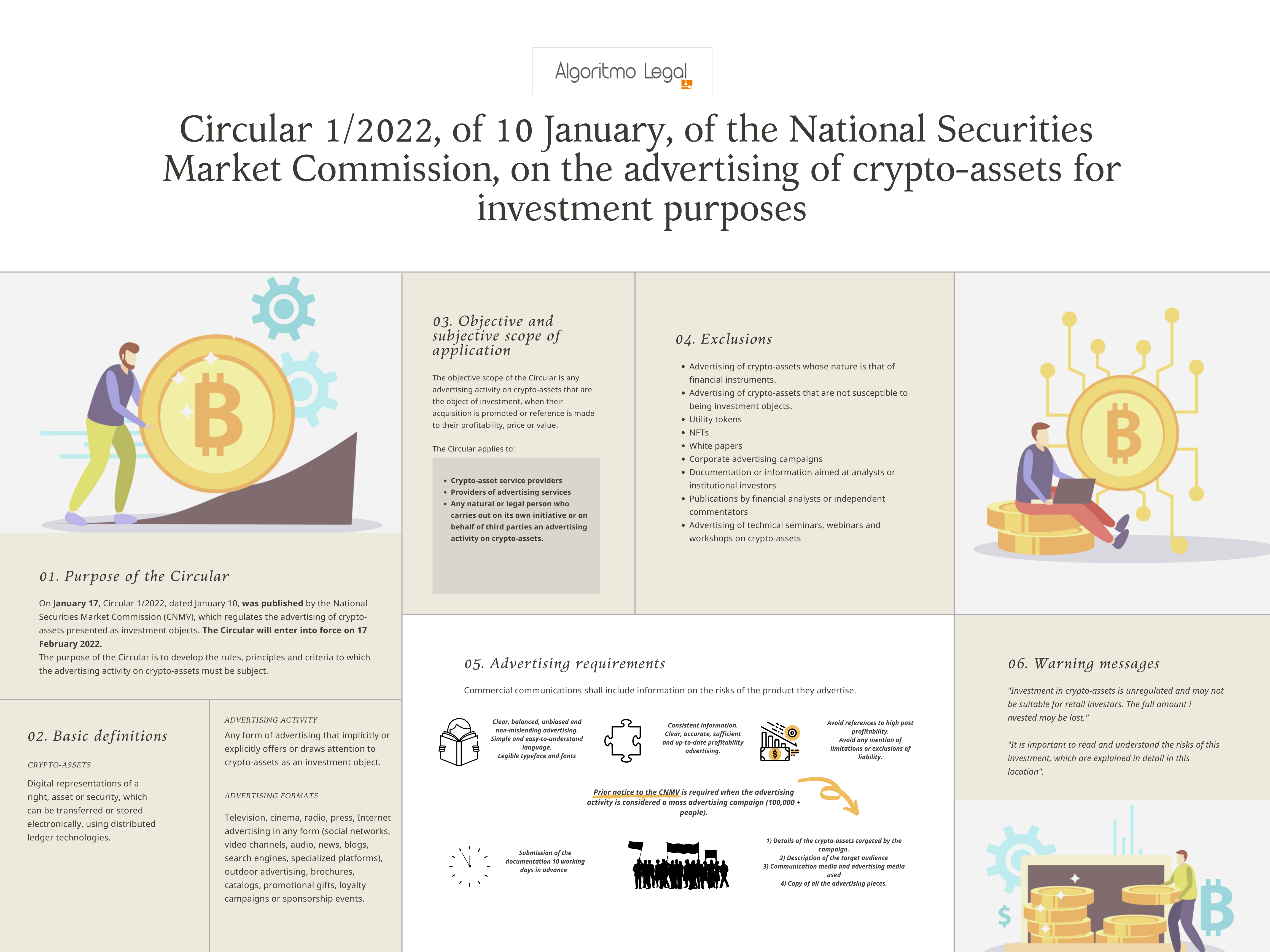

1. What is the purpose of the Circular?

Using the powers granted by Article 240 bis of the LMV, the CNMV has drafted the Circular to develop the rules, principles and criteria to which advertising activity on crypto assets must be subject.

In particular, the Circular delimits its objective and subjective scope of application, specifies the advertising activity that must be subject to a prior notification regime and establishes the tools and procedures that will be used to make the supervision of crypto-asset advertising activity effective.

The Circular should not be interpreted as a general regulation of crypto assets. In fact, it does not contain any rules on crypto asset products themselves, nor on their providers or their characteristics, rather it only regulates the requirements to be met by advertising activity aimed at offering crypto assets as a possible investment product.

2. Essential definitions of the Circular to be clear about

What is a crypto asset for the CNMV?

The Circular defines it as the digital representation of a right, asset, or security, which can be transferred or stored electronically, using distributed ledger technologies (e.g. blockchain), or other similar technology. This definition is virtually the same as that provided by Article 3 (1) of the Proposal for a Regulation of the European Parliament and of the Council on Markets in Crypto-asset (hereinafter, the “MiCA Regulation”).

What does it mean for a crypto asset to be the subject of a potential investment or to be offered as an investment product?

It means that its acquisition is promoted or that any reference is made to its current or future performance, price or value that may suggest an investment opportunity in the market, even though it may eventually be used as a medium of exchange.

What does advertising activity mean for the CNMV?

Advertising activity means all forms of advertising, regardless of the media and formats used (e.g. television, cinema, radio, press, internet or mobile advertising, all types of outdoor advertising, direct advertising, point-of-sale advertising, brochures, catalogues, promotional gifts, loyalty campaigns, sponsorship events, home visits, sponsored press articles or any other form of commercial communication).

Advertising should be understood as any form of communication made by a natural or legal person, public or private, in the exercise of a commercial, industrial, craft or professional activity, with the aim of directly or indirectly promoting the contracting of movable or immovable property, services, rights and obligations (Article 2 of Law 34/1988, of 11 November 1988, General Law on Advertising, Ley General de Publicidad).

The term “commercial communication” is defined as any form of transmission of verbal or visual information aimed at promoting, directly or indirectly, through texts, images and/or sounds, the crypto assets that are the object of investment.

An “advertising campaign” means the set of actions aimed at advertising a product through a single piece or a series of different advertising pieces, but grouped in time, even if not simultaneous, and related to each other, which are disseminated through various media or tools during a specific period.

The National Securities Market Commission defines a crypto asset as the digital representation of a right, asset or value, which can be transferred or stored electronically, using distributed registration technologies (e.g. blockchain) or other similar technology.

3. Objective scope of application of the Circular: advertising activity for crypto assets that are the object of investment

The Circular applies to advertising activity for crypto assets that are the object of investment, that is, any advertising aimed at investors or potential investors in Spain that implicitly or explicitly offers or draws attention to crypto assets as products of investment.

An advertising activity is presumed to be directed at investors in Spain when it is carried out through physical media in Spain, through Spanish media – including Spanish websites and domain names – and all those that are carried out in Spanish or other official languages, unless they contain measures that attest that the services or products promoted are not directed or accessible to investors in Spain.

4. Which crypto asset advertising activities are excluded from the objective scope of application of the Circular?

The following crypto asset advertising activities are not covered by the Circular:

- Advertising about crypto assets when these are of the nature of financial instruments included in the Annex of the LMV (the advertising of financial instruments is regulated in the CNMV Circular 2/2020, of 28 October, on the advertising of investment products and services, and in the Order EHA/1717/2010, of 11 June, on the regulation and control of the advertising of investment services and products).

- Advertising of crypto assets which, given their characteristics and nature, are not susceptible to investment.

- Advertising of crypto assets whose only use is digital access to a product or service, and which is accepted only by the issuer or by a limited set of commercial providers with which the issuer has a contractual relationship, and provided that there is no expectation of revaluation. The CNMV is referring here to the so-called “utility tokens”, defined by the MiCA Regulation as a type of crypto-asset used to provide digital access to a good or service, available through decentralized ledger technologies, and accepted only by the issuer of the token in question. Utility tokens typically offer their holder only a right to future access or enjoyment of the product or service that the issuing company will develop.

- Advertising of crypto assets that are unique and not fungible with other crypto assets, when they represent collectible assets, works with intellectual property or assets whose sole purpose is their use in games or competitions. The CNMV is referring to what are known as NFTs (Non-Fungible Tokens).

- The explanatory documentation for a new crypto asset issue. This is what is known in the industry as “white papers”.

- Corporate advertising campaigns, where no reference is made to crypto-assets or the provision of services related to them, and provided that the advertising messages included on the website of the legal entity carrying out the campaign comply with the provisions of the Circular.

- Documentation or information provided in presentations on a new issue of crypto assets provided that they are aimed solely at analysts or institutional investors.

- Publication on crypto assets issued by financial analysts or independent commentators if they are not sponsored or promoted.

- Advertising of technical seminars, webinars, and workshops on crypto-assets, provided that they do not promote investment in crypto-assets.

5. Subjective scope of application of the Circular: obliged entities

The Circular applies to the following entities when they carry out the crypto-asset advertising activities described in section 3 of this post:

- Crypto-asset service providers.

- Providers of advertising services.

- Any other natural or legal person that carries out, on its own initiative or on behalf of third parties, advertising activities on crypto assets. In this last group we can include influencers, football players, celebrities and other content creators who promote brands linked to crypto assets for the benefit of certain companies and provided that this activity has been remunerated.

6. How should obliged entities conduct advertising campaigns for crypto assets?

When designing advertising campaigns, obliged entities must consider the nature and complexity of the product, the characteristics of the media used and the target audience.

All marketing communications shall include information on the risks of the product being advertised. In particular, they should prominently display the following warning message: “Investment in crypto-assets is unregulated, may not be suitable for retail investors and the full amount invested may be lost”. They shall also include additional information on the general principles and criteria described in Annex I of the Circular, and, if applicable, on the technological and legal risks of crypto-assets where they are considered a high-risk investment product, as indicated in Annex II of the Circular, in which case the following text should be included: “It is important to read and understand the risks of this investment, which are explained in detail in this location”.

The general principles and criteria described in Annex I of the Circular are the following:

- Advertising should be clear, balanced, unbiased and not misleading, and should use simple and easily understandable language. In this regard, the inclusion of superlative or diminutive adjectives or expressions or adjectives indicating advantages of crypto assets should be based on objective and verifiable factors and data.

- The information must be consistent and may not contradict information or warnings provided by obliged entities to their customers.

- In advertising the profitability of a crypto asset, the information must be clear, accurate, sufficient, and up to date. If references are made to the advantages of a particular tax treatment, it should be made clear whether this is of a general or it depends on the customer’s personal situation.

- Marketing communications should avoid making references to high past profitabilities. Where this is done, information on past profitabilities should explicitly state the time period to which it refers and should not be provided in a partial or biased manner, nor refer to returns longer than 12 months. In addition, the terms in which each profitability is being expressed must be sufficiently visible, and historical profitability may not be the most prominent feature of the advertisement.

- Obliged entities must ensure that the marketing communication is understood. Disproportionate or false impressions or expectations, which may create an incentive to trade in the advertised crypto assets, should be avoided.

- Secondary information included in advertising should not contradict the main message.

- Commercial communications and other advertising pieces must be designed in such a way that they do not omit or conceal information. To this end, consideration should be given to the advertising medium used on each occasion, and if it imposes space or time limitations, reference should be made to alternative sources of information (e.g. including a QR code in the advertising message where the information can be read in more detail).

- Any mention of limitations or exclusions of the liability of the obliged entities for the content of the advertisement should be avoided. In the case of advertisements broadcast via social networks – e.g. by influencers – they are responsible for compliance with the provisions of the Circular when forwarding texts or content shared by a third party.

- The typeface and fonts used in the advertising message must be easily legible. If an audio or video format is used, it must be of sufficient length to convey the information clearly and completely.

Regarding the risks affecting crypto assets as high-risk investment products, Annex II of the Circular states the following:

- That both the value of the investments and the return obtained by the crypto assets being invested are volatile, and the entire amount invested may be lost. Consequently, keep in mind that these crypto assets are not covered by customer protection mechanisms, such as the Deposit Guarantee Fund or the Investor Guarantee Fund.

- Technological risks include the likely existence of significant failures in the operation and security of distributed ledger technologies; the possibility of losing all crypto assets as a result of a cyber-attack, as there is no alternative record of transactions in networks based on distributed ledger technologies; the anonymity inherent in crypto-assets may facilitate impunity for cyber-criminals who steal credentials or private keys; and entities that perform custody tasks for crypto-assets may cause the investor to lose everything in the event of theft or loss of private keys.

- Legal risks include: there is no legal obligation to accept crypto assets as a medium of exchange; in cases where the service provider is located outside the European Union, resolving disputes with the investor can be very difficult; and where the investor’s private keys are held in digital wallets controlled by a service provider (so-called “hot wallets”), the investor must be clearly informed of this situation, and the investor’s rights over these crypto-assets must be explained.

7. Is prior notification to the CNMV required to carry out advertising activities on crypto assets that are presented as products of investment?

The CNMV only needs to be notified of an advertising activity when it is considered to be a mass advertising campaign, i.e. when it is an advertising campaign aimed at more than 100,000 people, using any advertising media. Exceptionally, obliged entities may be required to give prior notice when they do not carry out mass advertising campaigns in the strict sense, when the CNMV so decides, due to the impact that such campaigns may have on the public.

If this is the case, obliged entities must provide the CNMC, at least 10 working days before the start of the advertising campaign, with an information document containing the general details of the campaign, such as the start and end dates, its territorial scope, a description of the target audience, a list of the media and supports used and a quantitative estimate of the number of people targeted, as well as specific information on the advertising pieces to be used.

This includes details of the crypto assets that are the object of the campaign, a description of the target audience, and a list of the media and advertising media used, as well as a copy of all advertising pieces with a different message or format.

This prior notification (communication) will allow the campaign to start 10 working days after its submission, unless the CNMV indicates otherwise. Failure to submit this documentation in advance will make it impossible to carry out the advertising activity.

Precisely, on February 17, 2022, the CNMV published on its website the prior communication model to be used when carrying out mass advertising campaigns, which you can download directly from said website.

Obliged entities must maintain a registry with all the aforementioned information and supporting documentation, with respect to the current advertising campaign and those carried out in the last two years. Therefore, the CNMV, as the supervisory body, must be informed in advance of any mass advertising campaigns for crypto assets that are intended to be launched, and may oblige obliged entities to rectify or withdraw them.

8. Evaluation

In 2021, this advertisement on Twitter became famous, featuring the well-known Spanish football player Andrés Iniesta, advertising the centralized crypto-exchange Binance.

Starting 17 February 2022, the date of entry into force of this Circular on the advertising of crypto assets, this type of advertising campaign will have to comply with the rules established by the Circular, in the terms we have outlined in this post.

With the approval of the Circular, Spain becomes a pioneering country in the world in regulating the advertising of crypto assets, when they operate as an investment product, something we believe is commendable and worthy of note. Explainability and transparency are crucial to ensure that users continue to trust in the advantages that distributed ledger technology can offer, and that investors can make their crypto assets profitable, knowing in advance the risks to which they are exposed.

You can read the Spanish version of this article here.

This article has been prepared by Ricardo Oliva León and Elena Almazán Salazar.